What Are Perpetual Futures?

Key Takeaways

Perpetual futures (or "perps") are a contract that lets a trader take a position on an asset's price, like a stock, commodity, or cryptocurrency, without owning it. Unlike traditional futures, perps never expire.

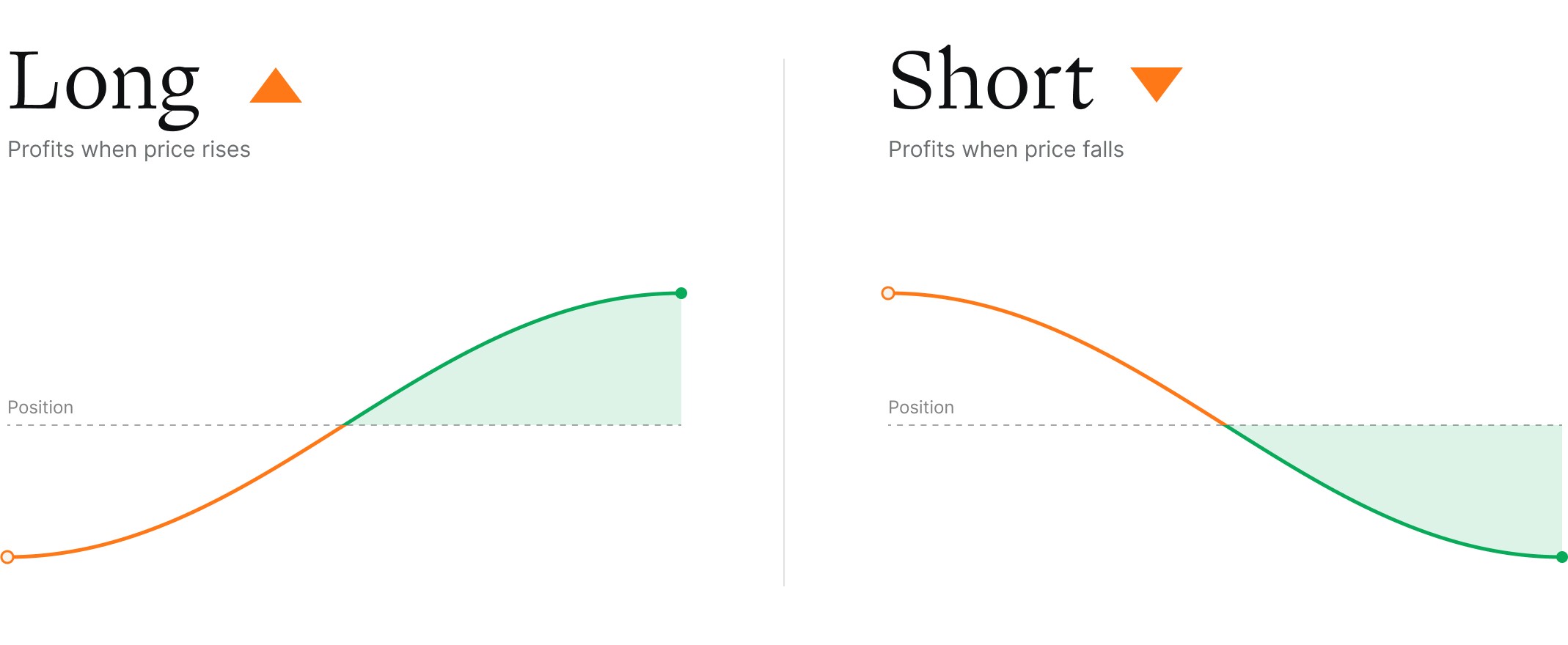

Perps let traders go long or short with leverage, profiting from price moves in either direction.

Leverage lets a trader control a larger position with less capital. At 10x leverage, $1,000 in collateral controls a $10,000 position, turning a 1% price move into a 10% swing on the trader's margin.

If a position's losses approach the collateral backing it, the exchange automatically closes the trade. This is called liquidation, and the trader loses their posted collateral. The higher the leverage, the smaller the price move it takes to trigger one.

The funding rate is a small periodic payment between long and short traders that keeps the perpetual's price aligned with the spot price of the underlying asset.

What are perpetual futures?

Perpetual futures are one of the most actively traded financial instruments in the world. Traders use them to take leveraged positions on everything from Bitcoin to crude oil to the S&P 500, going long or short on an asset's price without owning it, borrowing it, or managing an expiration date.

A perpetual future, often called a “perp” by traders, is a financial contract that lets traders speculate on the price of an asset without owning it outright. It looks and behaves like a traditional futures contract, with one critical difference: it has no expiration date.

Traditional futures contracts are among the oldest financial instruments in the world. The Dojima Rice Exchange in Osaka, Japan, widely considered the world’s first organized futures market, began trading rice futures in 1730. Today, they’re used to trade everything from crude oil to the S&P 500 index to gold. Every traditional futures contract has a fixed expiration date. When that date arrives, the contract settles and the position closes.

Perpetual futures work the same way. They track the price of an underlying asset, and traders can go long (expecting the price will rise) or short (expecting it will fall). The difference is that a perp can be held indefinitely. As long as the trader maintains enough collateral to back the position, they can keep it open for as long as they want.

Removing the expiration date unlocked sustained leveraged trading without contract rollovers. Today, perps trade 24/7 across global markets.

How is a perpetual future different from a traditional futures contract?

A traditional futures contract is an agreement to buy or sell an asset at a fixed price on a specific future date.

For example, a December corn futures contract priced at $4.50 per bushel locks in that price for the buyer. When the contract expires, it settles according to the exchange's rules: either through physical delivery of the underlying asset or as a cash payment for the difference between the contract price and the settlement price. Most futures are also marked to market daily, so gains and losses flow through accounts as the price moves, not only at expiration. Futures on crude oil, the S&P 500, gold, and other major assets all work this way, with fixed expirations that typically cycle monthly or quarterly.

A perpetual future works almost identically, except it never settles. There is no expiration date, no delivery, and no forced close. A trader can open a position and hold it as long as they maintain sufficient collateral.

That single change creates a cascading set of differences:

Eliminates rollovers: traditional futures traders who want long-term exposure must repeatedly close expiring contracts and open new ones in a process called “rolling.” Perpetual traders don’t deal with this.

Introduces the funding rate: with no expiration date to anchor the price, perpetuals use a small periodic payment between long and short traders (typically every 1 to 8 hours) to keep the contract's price aligned with the spot price of the underlying asset.

Enables 24/7 markets: traditional futures trade during exchange hours — the CME’s markets, for instance, close for about an hour each weekday and halt entirely on weekends. Perpetual futures trade continuously across global venues.

The first perpetual future was launched in May 2016 by crypto exchange BitMEX, with a Bitcoin contract called XBTUSD. The design solved a specific problem: traders wanted sustained leveraged exposure to Bitcoin without constantly rolling expiring contracts. Within a few years, perpetuals had become the primary venue for leveraged crypto trading worldwide.

How do perpetual futures work?

At the simplest level, trading a perpetual future works in four steps. A trader deposits collateral with an exchange. They use that collateral to open a leveraged position, either long or short. As the underlying asset’s price moves, their position gains or loses value in proportion. They close the position at any time. There is no expiration date forcing a decision. The only thing that can force a close is liquidation, which happens when losses exceed the collateral.

There are a few key mechanics worth understanding before making a first trade.

Going long and short

Every perpetual futures trade has two sides.

A trader goes long by buying a contract, expecting the underlying asset’s price to rise. They go short by selling a contract, expecting the price to fall. Profit and loss come from the difference between the opening price and the closing price, multiplied by the position size.

One of the reasons perpetual futures became popular is because of how simple shorting is. In traditional markets, short-selling a stock requires borrowing shares, posting collateral at a broker, and managing a complex process. In a perpetual futures market, a trader shorts by clicking “sell” instead of “buy” and the exchange handles the rest.

For example, a trader opens a long position on Bitcoin at $60,000 with $1,000 of margin at 10x leverage. That margin controls a $10,000 position. If the price rises to $61,000 (a 1.67% gain on the underlying), the position is worth $10,167, so the trader's $1,000 margin has grown by $167. That's a 16.7% return on their collateral. If the price falls to $59,000 instead, the trader is down 16.7%.

Holding the position through funding cycles costs a small amount per cycle (typically a fraction of a percent), and with $1,000 of margin backing a $10,000 position, a roughly 9% adverse move would put the position close to liquidation.

Margin and leverage

To open a position, a trader posts collateral called margin. With leverage, that margin can open a position much larger than itself. As in the worked example above, $1,000 of margin at 10x leverage controls a $10,000 position, and higher leverage amplifies both gains and losses further. Different exchanges offer different maximum leverage, typically ranging from 5x on conservative venues to 100x or more on aggressive ones. (For more on how leverage works across positions and venues, see our guide to leverage in perpetual futures.)

The funding rate

Because perpetual futures never expire, they need a mechanism to keep their price aligned with the spot price of the underlying asset. That mechanism is the funding rate: a small periodic payment exchanged between long and short traders every one to eight hours, depending on the exchange. When the perpetual's price trades above spot, longs pay shorts; when it trades below spot, shorts pay longs. Over time, that payment creates an economic pull that keeps the two prices in line. (For how funding rates are calculated, what typical rates look like, and how they affect held positions over time, see our guide to funding rates.)

Liquidation

If a position's losses approach the collateral backing it, the exchange automatically closes the trade. This is called liquidation, and the trader loses their posted collateral. In practice, exchanges close the position before losses fully consume the collateral; the exact threshold is set by each venue's maintenance margin rules.

The higher the leverage on a position, the smaller the price move it takes to trigger liquidation. At 50x leverage, a move of roughly 2% against the position can be enough.

What do traders use perpetual futures for?

Perpetual futures have become one of the most actively traded instruments in global markets because they solve specific problems for different types of traders. A few of the most common reasons are:

Leverage and capital efficiency: a small amount of collateral controls a much larger position, letting traders take directional exposure without tying up full capital. For example, a fund with $100,000 in collateral can express $1 million in directional exposure at 10x leverage and keep the remaining capital productive elsewhere.

Simplified shorting: shorting in traditional markets requires borrowing the asset from a broker and managing complex collateral mechanics. In a perpetual futures market, going short is as simple as going long — a trader clicks “sell” instead of “buy.”

24/7 access: traditional markets close. Perpetual futures never do. Traders can react to weekend news, overseas events, or major data releases the moment they happen, rather than waiting for markets to reopen.

Multi-asset exposure from one account: some perpetual futures venues, including newer DEXs like GTE, list contracts on crypto, equities, commodities, and indices side by side. A trader can go long Bitcoin, short oil, and hedge an S&P 500 position from a single interface.

Hedging existing positions: a trader who holds the underlying asset can open an opposite position in a perpetual future to reduce exposure without selling the original holdings. For example, a Bitcoin holder worried about a short-term price drop could short BTC perpetuals rather than liquidating their spot position.

Where can you trade perpetual futures?

Perpetual futures trade on two main types of venues: centralized exchanges (CEXs) and decentralized exchanges (DEXs). Centralized exchanges like Binance, Bybit, and OKX are the largest by volume, typically offering the deepest liquidity and lowest latency, with the trade-off that traders deposit funds into accounts the exchange custodies. Decentralized exchanges like Hyperliquid, dYdX, and Lighter let traders trade from a self-custody wallet, with trades settling on a blockchain. (For a deeper comparison, see our guide to centralized vs. decentralized perpetual exchanges.)

The gap between the two has been closing rapidly: perpetual DEX market share grew from 2.0% to 10.2% in just two years, with monthly volumes crossing $1 trillion for the first time in October 2025.

GTE is one example of a new-generation perpetual DEX. Currently in testnet, GTE is built on a central limit order book (the same model used by Nasdaq and the New York Stock Exchange) and offers contracts across crypto, equities, commodities, and prediction markets.